You sit at your desk, the ambient glow of the monitor casting long, cool shadows across your office. It is late, and the only sound is the faint hum of your laptop as you approve the final batch of monthly invoices. For years, this exact routine felt like a brilliant, weightless strategy. Paying independent contractors gave you agility. You avoided the heavy machinery of payroll and the sluggish paperwork of traditional employment.

But outside your quiet office, a quiet, sweeping regulatory shift is currently rewriting the rules of your business. You built a lean operation, bringing in talent exactly when you needed it, trusting the standard 1099 forms to keep you compliant. Recently, though, an unsettling tension has started pulling at the edges of that comfort.

If you check search metrics today, you will notice a massive, almost frantic surge in legal queries regarding contractor status. This is not a coincidence or a seasonal tax panic. It is the immediate fallout of a governing body changing its fundamental approach to oversight.

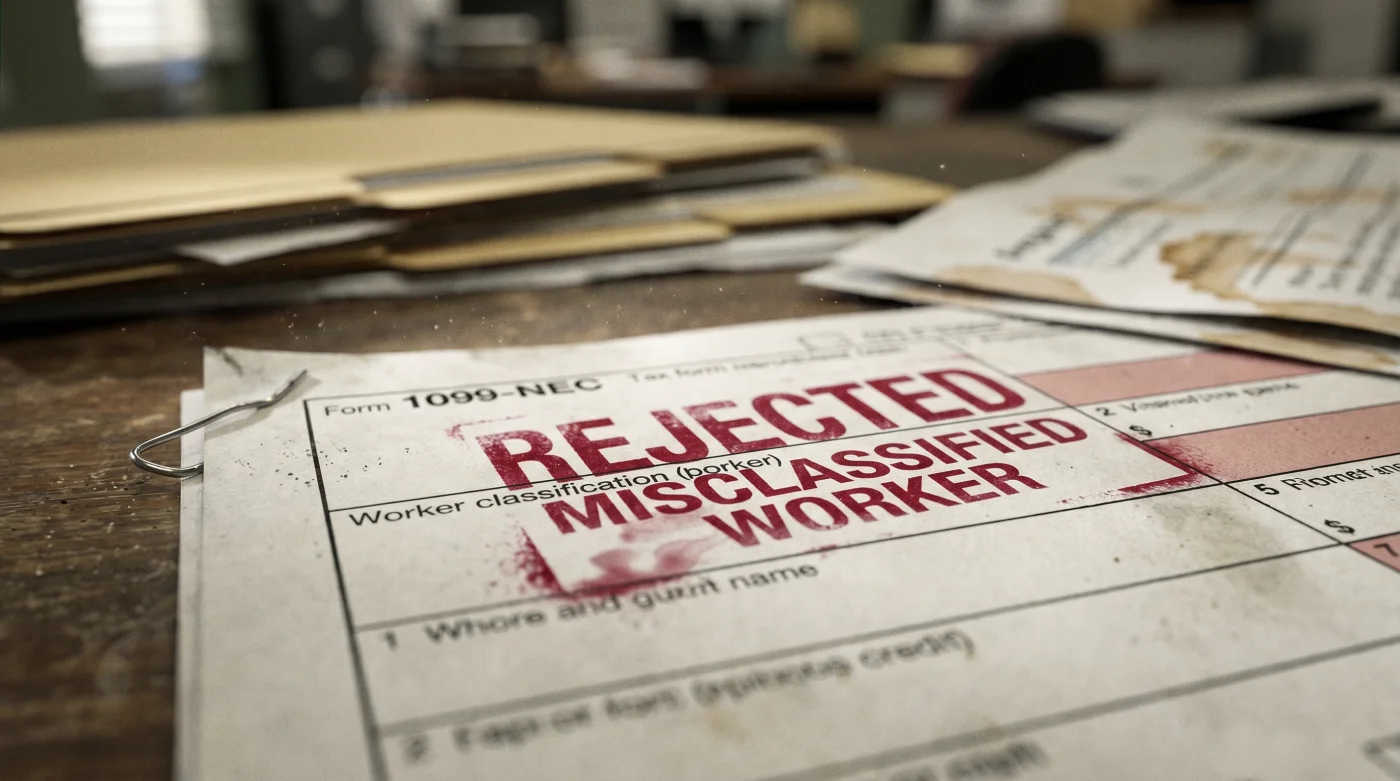

The Internal Revenue Service is no longer relying on random manual audits; they are deploying the brutal precision of algorithms to flag worker misclassification. What once required a human agent to notice an irregularity now happens in milliseconds, automatically cross-referencing your tax filings with state labor boards and corporate records.

The Invisible Tripwire and the Armor of Payroll

Think of your current worker classification not as a casual label you stick on a file folder, but as a load-bearing wall in the architecture of your business. If the foundation is mismatched, the entire structure is compromised. The myth we all bought into was that a signed freelance contract was an impenetrable shield. We believed that as long as the worker agreed to 1099 status, the government would look the other way.

That logic is entirely obsolete under this unprecedented digital dragnet. The new IRS algorithms are trained to hunt for behavioral and financial patterns that suggest an employer-employee relationship disguised as freelance work. The perceived flaw of W-2 classification—that it costs more and restricts your flexibility—must now be viewed through a completely different lens. Bringing your core workers onto actual payroll is no longer a financial burden; it is the ultimate defensive strategy, shielding your assets from existential tax penalties while building a fiercely loyal team.

- Warranty deed titles leave homes exposed to predatory liens

- LLC formation services mask steep recurring registered agent fees

- Building permit rejections stem from one missing structural dimension

- Flight cancellation compensation requires specific federal terminology for payouts

- Property line disputes rely on obsolete century old markers

Consider Sarah Jenkins, a 42-year-old forensic CPA based in Chicago. Last November, she received a frantic call from the owner of a mid-sized design agency. The owner had treated his graphic designers as independent contractors for six years without a single issue. Then, the new IRS algorithm flagged a minor discrepancy: the contractors were using company-issued email addresses and receiving exactly the same flat fee every Friday. Within three weeks, the agency faced a crippling audit for back taxes and uncollected payroll liabilities. Sarah spent months dismantling the damage, a process that cost the owner ten times what a proper payroll system would have required.

Profiling the Algorithmic Vulnerabilities

The machines scanning your records do not care about your intentions; they only care about data points. Different operational models trigger different digital red flags. You must examine your own setup to see where you are most exposed.

For the Lean Startup

If you rely heavily on remote fractional workers to build your product, you are a primary target. Algorithms immediately look for the duration and exclusivity of the relationship. If a developer bills you 40 hours a week for eighteen consecutive months and has no other clients, the system will flag them as a misclassified employee, regardless of what your written agreement says.

For the Brick-and-Mortar Operator

You might use contractors to clean your facility, handle daily maintenance, or even cover front-desk shifts. Here, the algorithm searches for integration into core operations. If the services these individuals provide are the primary way your business functions day-to-day, the IRS views them as employees. You cannot outsource your core operational dependency to a 1099 status.

For the Scaling Solopreneur

Making your very first hires often involves paying an assistant or a social media manager as a freelancer to keep things simple. The danger here lies in behavioral control. If you dictate their exact hours, provide their laptop, and require them to follow your specific operational handbook, you are leaving a glaring digital footprint of an employer-employee dynamic.

The Reclassification Protocol

Surviving this compliance sweep requires swift, deliberate action. Panic will only lead to administrative mistakes. Instead, approach your reclassification as a methodical upgrade to your business infrastructure. Follow these mindful steps to course-correct before a digital flag is raised.

- Audit your contractor agreements immediately. Remove any language that dictates specific working hours, mandatory training, or exclusive service requirements.

- Review your communication tools. Independent contractors should not have generic company email addresses or be mandated to use your internal project management software for their own internal processes.

- Evaluate financial independence. Ensure your contractors are invoicing you per project or deliverable, rather than receiving a fixed, salary-like payout every single week.

- Initiate the transition conversation. Approach workers who need to be reclassified with transparency, framing the move to W-2 as an investment in their long-term stability with your company.

Your tactical toolkit for this transition requires precision. Use IRS Form SS-8 cautiously—while it determines worker status, filing it alerts the IRS to your uncertainty. Instead, work quietly with a payroll specialist. Give yourself a 30-day window to migrate heavily integrated contractors to formal W-2 payroll. Set your new payroll systems to automatically calculate the employer side of Medicare and Social Security, removing the manual friction from your week.

Building a Resilient Foundation

When you stop fighting the current of regulatory oversight, a profound shift happens in how you run your business. Reclassifying your team is not a defeat; it is an act of operational maturity. The fear of an audit fades, replaced by the quiet confidence of knowing your foundation is solid.

You no longer have to worry about digital tripwires or algorithm updates. Your energy returns to your actual craft, rather than nervously managing the borders of tax compliance. By offering true employment to those who help build your vision, you foster a culture of trust and investment that no freelance contract could ever replicate.

The peace of mind that comes from a clean, compliant payroll system is the highest return on investment a business owner can buy.

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| Algorithmic Audits | The IRS now uses automated data cross-referencing to find 1099 anomalies. | Provides early warning so you can fix errors before a machine flags your account. |

| Behavioral Control | Dictating how and when a contractor works creates an employee relationship. | Clarifies exactly what management habits you must drop to stay compliant. |

| The W-2 Advantage | Moving core workers to payroll shields the business from back-tax liabilities. | Turns a stressful administrative chore into a strategic asset protection move. |

Common Compliance Questions

Will the IRS automatically fine me if I change a 1099 to a W-2 mid-year?

No, proactively transitioning a worker to W-2 status mid-year is generally seen as a corrective measure, not an immediate trigger for a fine. The danger lies in ignoring the misclassification until the algorithm catches it.Can an independent contractor still work 40 hours a week for me?

Yes, but the risk increases significantly. If they work 40 hours a week for you, they must maintain complete financial and behavioral independence, such as having their own tools and ideally other clients.Does a signed contract prove someone is an independent contractor?

A contract is merely a piece of paper. The IRS looks at the actual working relationship and behavioral facts on the ground, completely ignoring the contract if it contradicts reality.Is it true that paying someone less than 600 dollars protects me from rules?

The 600 dollar threshold only dictates whether you must issue a physical 1099 form. It does not exempt you from labor laws or worker classification standards.How long do I have to fix a misclassified worker situation?

You should act immediately. With data scanning happening in real-time across multiple state and federal databases, your window to manually correct your payroll structure is smaller than ever.